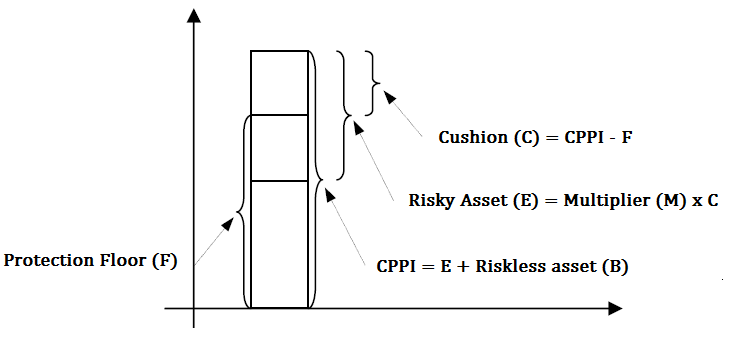

Constant Proportion Portfolio Insurance (CPPI)¶

In [1]:

import numpy as np

import pandas as pd

import edhec_risk_kit as erk

import matplotlib.pyplot as plt

%matplotlib inline

Run a Constant Proportion Portfolio Insurance (CPPI) strategy: ¶

- Keep exposure in a risky asset for upside potential, while ensuring capital preservation by increasing allocation to a safe asset if your portfolio value is nearing a set floor.

In [2]:

ind_return = erk.get_ind_returns()

# simulate returns from a safer asset, like bonds,

# using geometric brownian motion

safe_r = erk.gbm(

n_years=10,

n_scenarios=1,

mu=0.03,

sigma=0.015

).pct_change().dropna()

# retrieve telecom returns from 2005 to 2014

# some processing so it runs properly in run_cppi()

risky_r = ind_return.loc['2005':'2014', 'Telcm'].reset_index().drop('index', axis=1)

risky_r.columns = [0]

# CPPI with monthly rebalances

# m = cushion multiplier

backtest = erk.run_cppi(

risky_r=risky_r,

safe_r=safe_r,

m=2,

start=1000,

floor=0.7,

)

Plot performance of CPPI strategy (black) vs strategy of allocating 100% of portfolio to the risky asset (orange)¶

- Set protection floor F to 70% of the initial investment

In [3]:

fig, ax = plt.subplots(figsize=(12,6))

backtest['Wealth'].plot(ax=ax, color='k', legend=False)

backtest['Risky Wealth'].plot(ax=ax, color='orange', style='--', legend=False)

ax.axhline(1000*0.8, color='red', linestyle='--')

plt.show()

Explore how adjusting CPPI parameters affects floor violations ¶

How does increasing the cusion multiplier m from 2 to 3 affect floor violations? Notice in the above example, there were no floor violations in the above case with m=2

In [4]:

# CPPI with monthly rebalances

# m = cushion multiplier

backtest = erk.run_cppi(

risky_r=risky_r,

safe_r=safe_r,

m=3,

start=1000,

floor=0.7,

)

In [5]:

fig, ax = plt.subplots(figsize=(12,6))

backtest['Wealth'].plot(ax=ax, color='k', legend=False)

backtest['Risky Wealth'].plot(ax=ax, color='orange', style='--', legend=False)

ax.axhline(1000*0.8, color='red', linestyle='--')

plt.show()

With m=3, we had a floor violation during the '08 recession. Check what the portfolio value dropped to.¶

Remember our floor value was set to 80% of the initial 1000 investment = 800

In [6]:

backtest['Wealth'].min()

Out[6]:

Utilize a max drawdown constraint to create a moving floor. Set the floor value to 70% of max(peak, account_value)¶

In [7]:

# with m=3, floor value being 70% of max(peak, account_value),

# max allocation to risky assket is 3*(100-70) = 90%

backtest = erk.run_cppi(

risky_r=risky_r,

safe_r=safe_r,

m=3,

start=1000,

riskfree_rate=0.02,

drawdown=0.3

)

In [8]:

fig, ax = plt.subplots(figsize=(12,6))

backtest['Wealth'].plot(ax=ax, color='k', legend=False)

backtest['Risky Wealth'].plot(ax=ax, color='orange', style='--', legend=False)

ax.axhline(1000*0.8, color='red', linestyle='--')

plt.show()

Summary of CPPI's returns¶

In [9]:

erk.summary_stats(backtest['Wealth'].pct_change().dropna())

Out[9]:

Summary of 100% Telecom returns¶

In [10]:

erk.summary_stats(backtest['Risky Wealth'].pct_change().dropna())

Out[10]:

CPPI strategy provided much better risk protection¶

- Max drawdown was halved,

- Negative skewness reduced,

- VaR and CVar near halved

- Higher Sharpe ratio

- Much less fat tail on distribution of monthly returns (kurtosis)

Although, overall, it underperformed because of the run from 2009-2015